Product ID: UCMIG25A2028

Report ID:

UCMIG25A2028 |

Region:

Global |

Published Date: Upcoming |

Pages:

165

| Tables: 55 | Figures: 60

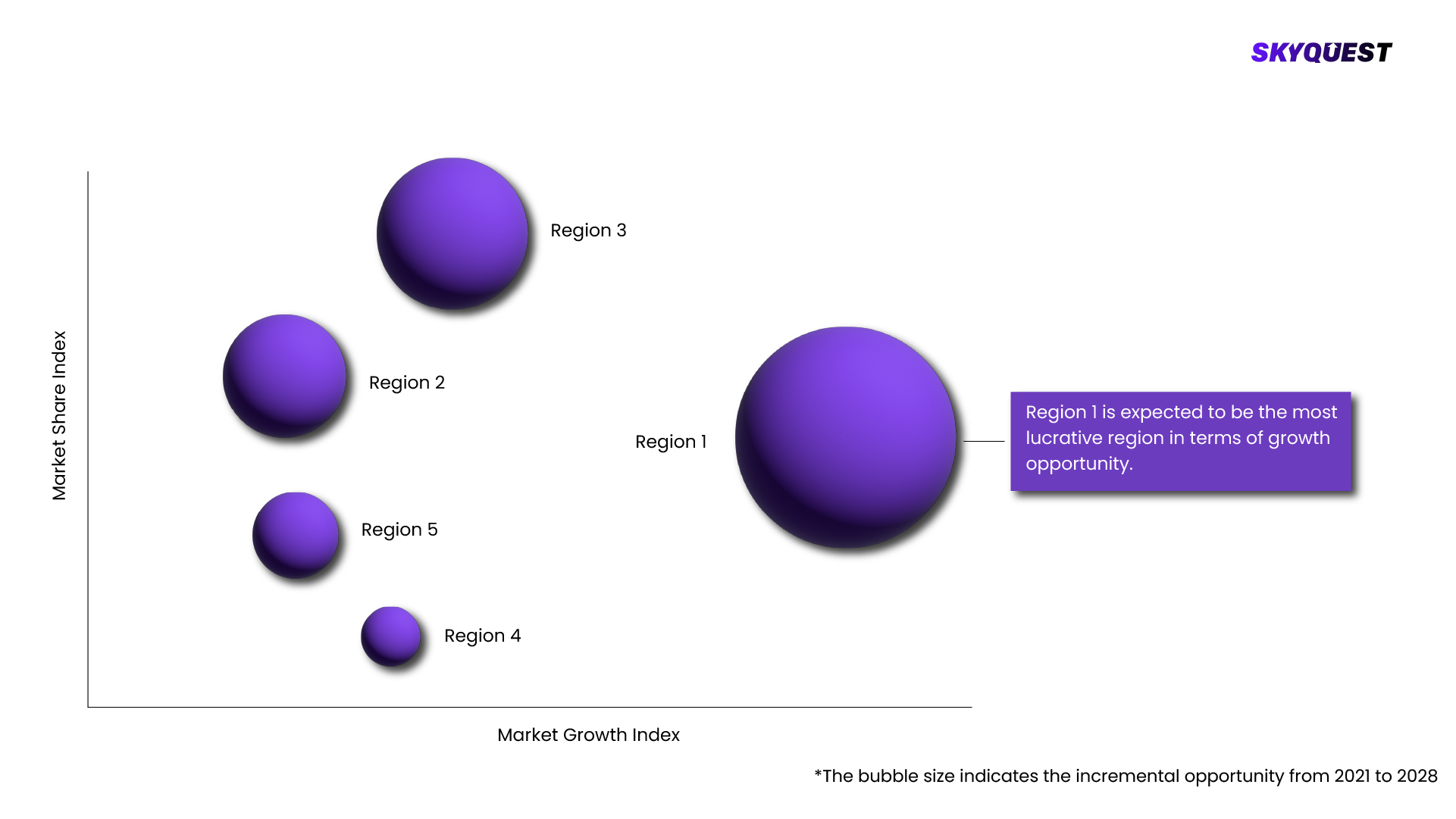

Automotive Simulation Market is being analyzed by North America, Europe, Asia-Pacific (APAC), Latin America (LATAM), Middle East & Africa (MEA) regions. Key countries including the U.S., Canada, Germany, France, UK, Italy, Spain, China, India, Japan, Brazil, GCC Countries, and South Africa among others were analyzed considering various micro and macro trends.

Our industry expert will work with you to provide you with customized data in a short amount of time.

REQUEST FREE CUSTOMIZATIONWant to customize this report? This report can be personalized according to your needs. Our analysts and industry experts will work directly with you to understand your requirements and provide you with customized data in a short amount of time. We offer $1000 worth of FREE customization at the time of purchase.

Report ID: SQMIG25A2272 | Region: Global | Published Date: Upcoming | Pages: 223 | Tables: 55 | Figures: 60

Global Automotive Electric Power Steering Market

Report ID: SQMIG25A2248 | Region: Global | Published Date: Upcoming | Pages: 221 | Tables: 55 | Figures: 60

Global Automotive Air Conditioning Market

Report ID: SQMIG25A2266 | Region: Global | Published Date: Upcoming | Pages: 218 | Tables: 55 | Figures: 60

Global Automotive Solenoid Market

Report ID: SQMIG25A2211 | Region: Global | Published Date: Upcoming | Pages: 222 | Tables: 55 | Figures: 60

Global Automotive Hinges Market

Product ID: UCMIG25A2028

USA (+1) 351-333-4748

USA (+1) 351-333-4748